Blog

What I Got Right (and Wrong) about Crypto in 2020

12/29/2020

It’s been a cold winter in crypto-land for the past year or so, but with bitcoin recently breaking back above $5,000, some folks think they are seeing the green shoots of spring. I think these folks are right…to some extent. I believe spring is coming, but it’s not coming to evenly to all parts of the land.

The euphoria of the 2017 crypto bull run ushered in a rush of activity in the space — some creating innovations that could change the world, and unfortunately, others sprinkling “blockchain” on everything and just trying to grab their piece of crypto riches in the frenzy. The cold of winter has separated out what is real…and what is not. This has led us to where we are today — on the verge of spring in some areas of crypto-land, while other areas are likely to remain in the deep freeze of winter (and a couple where spring will come, but need more time).

In this post, I visit 9 of the major areas of crypto-land, and across 85 theses, break down were they fall on the following spectrum:

A. Green Shoots — There are real green shoots in these areas, and spring is on its way.

B. Punxsutawney Phil (Sees His Shadow) — Hunker down for a longer winter…these areas need some more time before spring.

C. Deep Freeze — These are going to remain in the deep freeze of winter for a while.

(With a caveat to these broad categorizations that even in areas where there are green shoots there are also some frozen spots, and vice versa)

Before diving into these specific areas, my 2 core crypto theses:

1) The fundamental innovation of crypto* is that, for the first time ever, parties anywhere in the world can transfer value without the need for a trusted third party.

2) This is a once in a generation technological innovation which will change the way value is stored and transferred.

*I use the phrase “crypto” to mean the use of distributed consensus ledgers (blockchains) to transfer units of value recorded on these ledgers (BTC, ETH, etc.)

And now, on to the remaining 83…

3) Adoption of crypto in markets with hyper-inflation continues to gain very strong momentum…and is just getting started.

4) Using crypto as a store of value will come before use as a medium of exchange or unit of account.

5) Over time, I expect merchants in countries with rapidly depreciating fiat currencies to accept crypto (and even price in crypto), as they don’t want to be the bagholder stuck with the worthless local fiat currency.

6) Widespread adoption of crypto in these areas will be dependent on widespread internet access & mobile adoption, education, improving user interfaces, scaling to allow a high number of fast transactions (likely via layer 2 solutions such as Lightning), and decreased price volatility (or use of stablecoins).

7) Crypto payments to emerging markets could unlock significant value for the global economy and raise standards of livings in emerging markets.

8) Getting crypto in the hands of people in markets with hyper-inflation is a clear win-win for everyone. People in these areas need a better currency (and often need financial assistance), and the crypto community needs crypto to be actually be used in the world. Supporting initiatives like #AirDropVenezuela is a great way to work towards these goals.

9) Bitcoin (+ level 2 scaling) continues to be the most likely asset to fulfill these promises, but that is not a forgone conclusion.

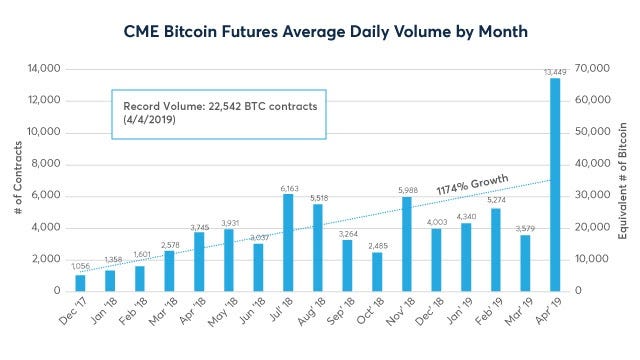

10) The herd (institutional investors) is coming. However, they are arriving in a steady saunter and not the thundering stampede some expected.

11) The great infrastructure buildout is happening — We are currently experiencing an infrastructure build that will usher in the next wave of participants into this market.

12) Despite this progress, the current market structure is capital inefficient and is likely to change.

13) Custody and settlement will increasingly be separated from exchanges.

14) One, or a small number, of the largest custodians will establish themselves as the “DTCC of crypto”. They will hold a large portion of crypto assets, and transfers of these assets will increasingly be recorded in the records of these custodians, without the need to move assets out of cold storage.

15) “Prime Brokerage” services will continue to emerge — intermediaries who provide access to markets, leverage, ability to short-sell, etc.

16) Prime brokerage can be a capital-intensive service, and to be provided well at scale, will likely need to be provided by either startups raising very large amounts of funding, or larger financial institutions.

17) The largest and most trusted financial institutions will (eventually) come into the market, particularly in custody and prime brokerage roles.

18) Crypto will have a dramatic impact on some traditional markets. The most significant impact will likely occur in FX, where the rise of stablecoins will also give rise to a new FX market, offering 24/7, instant, low-cost conversation between currencies.

19) ETF’s will be approved (at some point). When a Bitcoin ETF is approved is highly uncertain, but when it is, will signal a titanic shift in the market as investors will be able to access crypto in a product structure they are very familiar with, and is offered through all major brokerage platforms and advisers.

20) Tax loss harvesting will become much more common in crypto. This is currently a big missed opportunity for investors, and automated tools will make this commonplace (much like robo-advisors have in traditional markets).

21) Stablecoins are likely to emerging as a new global money transfer rail, although they face potential competition from new centralized payments systems.

22) In the near-term, fiat-backed stablecoins (fiat held in bank accounts backing coins) are more promising than truly decentralized stablecoins (such as Maker Dai).

23) Maker Dai is a complex, but brilliant and beautiful system, however…

24) It’s also an unproven R&D project at this point (as are all other fully decentralized stablecoins), as shown by recent difficulties maintaining its peg and internal turmoil. Companies and individuals are not going to trust truly large sums of money in this sort of system in the near-term.

25) The value in fiat-backed stablecoin systems does not come from them fully using the fundamental innovation of crypto (since there is a trusted third party involved in holding the fiat), but instead from the fact that they allow the creation of a new global money transfer rail that is completely accessible (to anyone with a crypto wallet), and interoperable across currencies (users can directly access and exchange any fiat currency).

26) A fiat-backed stablecoin system can also be more efficient (fast, free, 24/7) than current money transfer rails (but a better centralized system could also hypothetically offer these efficiency gains).

27) In assessing the potential of stablecoins as a new global money transfer rail, I look at A) the characteristics of an ideal global money transfer rail, and B) the various ways this new money transfer rail could be provided (both centralized and decentralized).

28) The ideal new global money transfer rail would offer:

29) There are several parties that could provide this solution, and they could offer it in a centralized or decentralized manner. The candidates to offer this (from least likely to most likely) are central banks, commercial banks, and large global tech / crypto companies.

30) Coordinated central banks could hypothetically provide these new rails, but are very unlikely to do so.

31) Large commercial banks are also candidates to provide this, but don’t provide a complete solution.

32) Large, global consumer technology and crypto companies may be the best positioned to provide new global money transfer rails (with records either kept on centralized databases, or a distributed consensus ledger (“DCL”)).

33) The hurdle of one company meeting worldwide financial regulations can be eased in a system in which there are different issuers of different fiat-backed stablecoins in different countries (must be DCL / decentralized system).

34) It seems that a new global money transfer rail utilizing stablecoins will emerge, in an elegant way in which:

35) In this multi-issuer scenario, centralizing the storage of coins with one custodian still offers a marginal benefit for use cases where instant transfers are required (since on-chain transactions are not completely instantaneous).

36) Even though I envision various stablecoin issuers in different countries, I believe there will only be a small number (1–2) dominant stablecoin winners for each currency.

37) Crypto regulation is still quite unclear, but regulatory certainty is continuing to emerge as various regulators around the world provide more guidance.

38) I am hopeful that smart regulation will clean up much of the bad behavior in crypto-land and fortify where crypto interacts with the traditional financial system, while allowing innovation in the ecosystem to continue to develop.

39) Compliance solutions will be one of the biggest opportunities for startups (and existing regulatory compliance companies) in the coming years.

40) Blockchain analysis to determine where crypto assets are being used by “bad actors” is inevitable…and that is ok.

41) If my thesis for the rise of stablecoins is right, this will be particularly relevant for these coins, as the redeem-ability of specific coins may be suspended if they are identified to be interacting with known bad actors.

42) I think this could be a good system to allow widespread use of stablecoins freely around the world, while still protecting the financial system from misuse (as it puts the regulatory hurdles primarily around the create/redeem process, and not on every transaction).

43) There will be a correlation between how tightly regulated crypto assets are and their use by regulated institutions.

44) Fiat-backed stablecoins will be the most tightly regulated, and most used by regulated institutions. Anonymous crypto assets (ZCash, Monero, etc.) are by design the most difficult to regulate and will be the least used by regulated institutions. Bitcoin will be in the middle. There will be options for everyone on the regulated / censorship-resistant spectrum.

45) Much of the most innovative work in crypto is being done around decentralized finance (DeFi) — i.e., utilizing smart contracts to offer trustless financial services (exchange, lending, insurance, etc.).

46) In the near-term, DeFi projects will largely continue to be fascinating research projects…widespread, real-world adoption will be slow to materialize.

47) Outside of the crypto community, no one generally cares if a solution is centralized or decentralized. They only care if the solution solves their problems better than current solutions.

48) Currently, there are few situations were DeFi solutions are solving a problem better than a centralized solution. Additionally, user interfaces for DeFi solutions are generally much worse than their centralized counterparts…which creates a huge barrier to DeFi adoption.

49) The use case for decentralized exchanges is developed markets is unclear, particularly as centralized exchanges become more trustworthy (e.g., by separating custody from the exchange, and/or providing proof of reserves).

50) Where most DeFi solutions (including decentralized exchanges) have their most clear potential value proposition is in emerging markets.

51) Cryptocurrencies need to gain adoption for their basic currency uses (store of value, medium of exchange) before more complex decentralized uses (e.g., decentralized lending) will take hold at scale.

52) The decentralized application I expect to get the most traction in the near-term is decentralized lotteries.

53) Within the next few years, there will be global, billion-dollar lotteries running on smart contracts.

54) These lotteries will be unstoppable (at the smart contract level), and governments will need to react to these developments. (e.g., by looking to restrict access to the interfaces that interact with the contracts?)

55) With the ICO market dead (more on that later), interest has turned to the tokenization of more traditional assets. (stocks, real estate, etc.)

56) The general pitch for tokenization of everything is that it allows smaller portions of assets to be traded (e.g., a fraction of a property), provides greater liquidity for these assets, and enables the democratization of finance by allowing individuals to invest in more assets.

57) To assess these claims, we need to look at what DCL’s are actually enabling that was not previously possible by keeping ownership records on a central database.

58) For most assets, it does not seem that tokenization is an inherently better way to track ownership records (vs. a centralized database).

59) An argument could be made that crypto exchanges have already onboarded very large numbers of users, and thus tokenizing new assets is the way to get these assets in front of these users (i.e., it is a distribution advantage, not a technology advantage).

60) I am hopeful that longer-term we will get to the tokenization of more assets and financial instruments, and that value of this model will come from not only the potential distribution advantage, but also from technological benefits decentralizing the tracking of ownership.

61) The ICO market is dead.

62) In many (most?) ICOs, the token was completely unnecessary.

63) Most ICO’d coins have no value capture mechanism (other than a weak hope that they would have “utility” within a closed system).

64) Much of what was issued in 2017/2018 was nothing more than commemorative coins — the main utility of which will be to give us something to look at and remember the crazy times we had during this period.

65) IEOs are renamed ICOs.

66) Many companies that did ICOs are realizing that their coins are not needed, and are trying to gracefully pivot their business models away from them.

67) Turns out the “business model” of 1) developing open source software, 2) adding a token, 3) profit …was largely a fallacy.

68) I don’t buy The Fat Protocols Thesis. More value will accrue at the application layer than the protocol layer.

69) Luckily, there are proven models for monetizing open source software (e.g., Red Hat) — providing services, hosting, and building enterprise versions. Expect to see a lot more of this going forward.

70) I DO expect to see new coins come on to the market that are valuable. These will either be new currencies (to challenge BTC, ETH, LTC, XMR, etc.), or that have legitimate value capture mechanisms (staking, rights to cash flows, etc.).

71) The dream of using bitcoin for purchases in developed markets (“buying coffee with bitcoin”) will continue to be just a dream in the near-future.

72) Merchant payment systems in developed markets work quite well.

73) There is little customer incentive to pay for items with BTC (or any digital asset) — using credit/debit cards is easy, and rewards points are great.

74) Merchants have some incentive to accept crypto since interchange fees are high, but they do not want to receive BTC (or any digital asset).

75) The best chance for using crypto in developed markets is using stablecoins + customer incentives provided by merchants.

76) However, the marginal benefit of this to merchants, weighed against the challenges of changing their payment processes, and incentivizing consumers enough to change their payment behavior, means this use case is likely going to remain in the cold of winter for a while.

77) Most “enterprise blockchain” solutions make zero use of the fundamental innovation of crypto (transferring value without the need for a trusted third party), and are better served by centralized databases.

78) Putting tomatoes (and other various fruits and vegetables) “on the blockchain” is probably the most egregious example of something that does not need a blockchain.

79) If you can replace the word “blockchain” with “database”, use a database.

80) As the head of blockchain for a major consulting firm told me, “most companies are realizing they don’t need a blockchain, but they are using this opportunity to modernize and digitize their business.”

81) Even in the dark deep freeze of the enterprise blockchain winter, there are a few companies that are utilizing crypto’s data anonymization and value exchange futures to disintermediate middlemen and create significant business value. There will be innovative “blockchain inspired” concepts that emerge from all of the enterprise blockchain work…and even some enterprises actually using real blockchains.

82) Spring is coming to crypto-land. It may not be imminent, but it is coming.

83) I expect spring to come first in the areas of Emerging Markets Usage, Investing & Trading, Stablecoins as New Global Money Transfer Rails, and Regulatory Compliance Solutions.

84) Decentralized Finance and The Tokenization of Everything will continue to develop in hibernation for a while.

85) ICOs, Buying Coffee with Bitcoin (developed market merchant payments), and Enterprise Blockchains will remain in the deep freeze of winter.

Credit goes to Ryan Selkis and Arjun Balaji for their much more eloquent lists of crypto theses which inspired this one.

If you are working on something interesting in the space, or just want to tell me how wrong I am about these theses, send me a DM @TheChicagoVC.

Peter Johnson is a Principal at Jump Capital, where he leads their investments in the fintech and crypto sectors. Since joining Jump Capital in 2013 as their first employee, he has invested in 50+ companies, including many leading crypto companies.

Jump Capital is a venture capital firm specializing in series A/B and growth stage investments. Jump invests in data-driven companies across the fintech, IT infrastructure, enterprise SaaS, and digital media sectors. Jump Capital is also affiliated with the Jump Trading Group, one of the largest proprietary trading firms in the traditional and crypto markets.

The opinions expressed herein are my own, and do not represent the opinions or views of Jump Capital or the Jump Trading Group or its members.